Leticha and the debt trap

A case study of how vulnerable people are preyed upon

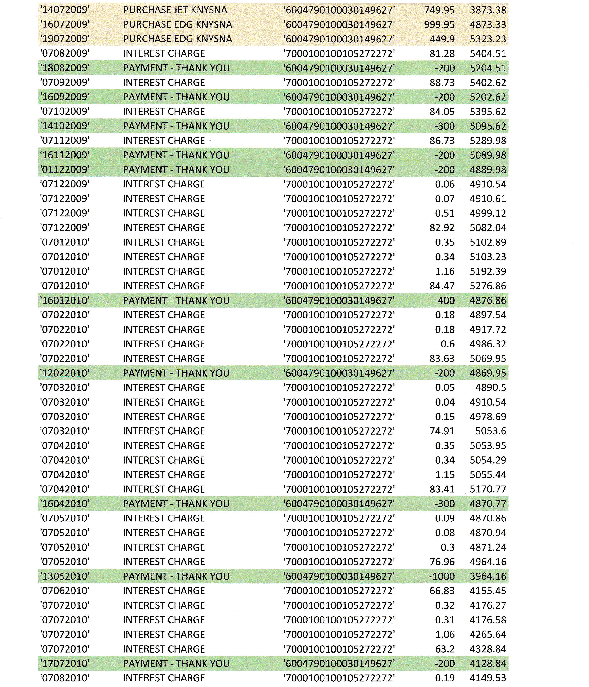

When your only income is a state Disability Grant of R1,500 per month, every rand counts. Ten years ago mentally challenged Leticha Marinana opened a credit account to buy clothes at Edgars, South Africa’s largest fashion group. Over the first three years she bought R10,497 worth of items, then never used her card again. With interest and charges she’s paid back R16,217 in monthly payments from her disability grant, but she was still being harried for a further R4,798.

Leticha is 39 and lives in Knysna on the scenic Garden Route. Not that she sees much of the tourist town voted second favourite city in Africa by Condé Nast Traveler, for Leticha is intellectually disabled and rarely leaves the timber RDP house in Khayalethu South that she shares with her 72-year-old widowed mother.

To pass the days, Leticha does the cooking and watches a lot of TV, the highlight being 9pm on weekdays when she escapes into the fantasy world of the SABC2 soapie Muvhango. It’s a relief from her once-tranquil real life, which has been spinning out of control since she got caught in a debt trap.

Nearly half the population’s in debt. Figures released by the National Credit Register for the first quarter of 2016 show that credit bureaux have files for 23.9 million credit-active customers, 9.5 million of them with records that are “impaired”, or in arrears on repayments. Total gross debtor’s book stood at R1.7 trillion.

One of the provisions of the 2007 National Credit Act was to prevent reckless lending. But the all-important affordability assessments were left to credit providers, using their own criteria. Last year, the National Credit Amendment Act compelled them to check applicants’ bank statements or salary slips, as well as use a “minimum expense norms table” to calculate affordability. Too late for Leticha.

From a baby, Leticha has suffered from hydrocephalus – water on the brain – a condition that can lead to developmental, physical and intellectual impairments. She dropped out of school in grade 9 and her doctor at Knysna Provincial Hospital told her she could never work. When she was 16 she underwent neurosurgery at Groote Schuur Hospital in Cape Town and at 19 was given a permanent Disability Grant, which was then R450 per month.

Her late father was a gardener on a pitiful wage and the family, like so many others, relied on credit for the necessities of life. Leticha’s mother had an account at Beares furniture store in Knysna and Leticha opened an account there too, buying a hi-fi, television and fridge for the house, paying off the R14,000 total at R250/month with her disability grant.

She says her good credit record at Beares “qualified me for Edgars for clothes”. So in August 2006 – the year before the National Credit Act with its limited protection came into effect – she applied to Edgars for credit, giving the disability grant, by then R820/month, as her sole income.

Under the affordability table in last year’s Amendment Act, that amount would have precluded her from getting any credit at all. However, back in 2006 Edgars considered it sufficient to give Leticha a 20-month interest-bearing plan with opening credit of R2210.

She used her Edgars card for just 11 months, making purchases totalling R10,497. Then there were unrequested extras, such as Club Classic with funeral benefit, for which her account was debited R877 – R20/month for nearly four years – before Leticha realised and cancelled it. She already had funeral cover with Doves.

Edgars, along with other big retailers including CNA and Boardmans, is owned by cash-strapped Edcon, presently carrying a R22 billion debt burden itself. In June 2012, in an attempt to ease its debt, Edcon sold its debtors’ book of more than 3.8m credit clients to Absa for R10 billion – and Absa took over as Leticha’s credit provider. Edcon’s credit sales fell by 8.3% in the second quarter of 2014 as Absa tightened up on what the bank considered had been Edcon’s lax credit granting.

For her R10,497 purchases, Leticha has repaid R16,217 – R3,911 of it in interest. Under Absa, interest was replaced by an “agent’s collection fee” of just a few rands a month. But despite numerous monthly payments of R100 over the next nearly four years, by this April the outstanding amount on her account still stood at a formidable R4,798. “It just never went down,” says Leticha.

It got worse. In 2010 Edgars was added to rival retailer Foschini’s financial marketing network and Leticha became a target in an “invitational mailing” aimed at expanding Foschini’s customer base. She took the bait and that December opened an account with Foschini, carrying an opening interest rate of 22%.

To JSE-listed Foschini Group, known as TFG, Leticha again declared her disability grant – now increased to around R1,100/month – as her sole income, and provided a confirmatory payment slip. Her application was approved and over the next six months, in two purchases, she bought clothes totaling R1,146. Since June 2011, she has not used her Foschini card again. But for the last five years she has made regular monthly payments to Foschini from her disability grant. TFG’s own records show that the repayments total R5,396.

Despite this, a statement in April this year informed her that she still owed a further R2,618.

How, asked her mother, could this be possible? The answer lies partly in an assortment of magazines that for years had been arriving from Foschini every month. With titles like Sports/Soccer and Club X for teenagers their contents were of no interest to Leticha. She finally discovered why her account balance never went down, staff at another Foschini outlet, Fashion Express, told her that she had been paying for these magazines.

With a Power of Attorney from Leticha I wrote to TFG chief executive Doug Murray asking him to look into Leticha’s case and explain why she had been given credit when she was on disability of (then) R1,100/month.

Murray’s office referred the case to TFG’s Sharief Allie, senior manager – credit policy in financial services. Allie quoted the National Credit Act: “The purpose of the act is to promote the development of a credit market that is accessible to all South Africans and particularly to those who have historically been unable to access credit.” Allie added: “The NCA does not regulate a minimum income requirement for the industry … TFG assessed Ms Marinana using its own assessment mechanisms.”

Attorney Stephen Logan, a credit law expert who chaired the technical committee that wrote the new affordability assessment regulations in last year’s National Credit Amendment Act, comments: “I think it’s dangerous to grant credit to someone who’s on a disability grant. It’s clearly something that could potentially be reckless. If you have that sort of income you have basically no discretionary income.”

Foschini’s Allie said their records showed that Leticha had subscribed to four magazines from April 2011 to November 2014. That amounted to R3,677. Other add-on charges were lifetime interest of R1,818, lifetime account insurance of R245 and lifetime collection charges of R898. Total outstanding balance on Leticha’s account at 29 August 2016 was R2,391.

But Leticha maintains she never asked for the magazines. Allie maintained that she did and that they were detailed on monthly statements. He said that “with Ms Marinana’s written consent, we can provide you a call recording between Ms Marinana and the salesperson (it’s in IsiXhosa).”

Leticha signed another Power of Attorney and we asked for the recording, as well as copies of three of her monthly statements detailing the magazines and their cost.

Silence.

Then an unexpected letter from Chantal Adler, legal adviser to TFG Financial Services. After a thorough investigation they believed that Foschini Retail Group (TFG) at all times acted correctly when they granted an account to Ms Marinana. “However, as it is not in our interests to have unhappy customers, and as we note that she made a concerted attempt to pay her account, as a gesture of goodwill we have made a decision to write off Ms Marinana’s outstanding balance and will subsequently be closing her account. She will receive no further demands for payment from TFG.”

Edcon, owners of Edgars, is itself struggling to reduce net debt of R22 billion in an ongoing restructuring programme. Our complaint to chief executive Bernie Brookes was passed to Alicia Naidoo, Customer Service Manager. Naidoo said they were unable to trace Leticha’s 2006 credit application to confirm she was on disability “due to the time frame that has passed”. She requested that Leticha provide “disability documents” and an affidavit confirming that she “has no source of income in order for us to assist her with an amicable situation”.

We produced slips showing a number of disability grant payments, as well as an affidavit confirming that due to her disability Leticha is unable to take paid employment.

Naidoo’s response: “The credit provider [Absa] has stated that the information is insufficient.” There was no hard proof that Leticia was on disability, the bank ordained. The R4,798 debt remained.

Edcon’s Alicia Naidoo was unhappy with Absa’s stance. She says: “I have advised [Absa] that the individual has been under disability for a considerable number of years. I have requested an escalation on behalf of Ms Marinana as I was not happy with the findings.”

In a push for evidence that Absa might accept, we paid a visit to Customer Services at Edgars in Knysna. This revealed a mass of early information about Leticha still on their system. Finally, a screen shot popped with the missing evidence: under Leticha’s Employer it stated Disability Grant.

We forwarded the screen shot to Edcon’s Naidoo who made her own decision, regardless of what Absa might say. “I have updated the status to reflect the Disability Grant under employer to ensure that no further actions be taken against the account. I will revert with the feedback,” she said.

To clinch things, the South African Social Security Agency confirmed that Leticha “has been on disability since 21 May 1996.” An official looked up the amount of the grant then – R450/month.

Last word from Edcon’s Naidoo: “Great news! We will clear out the balance on the account. We are busy with the process and will revert once it has been completed.”

Leticha is free of debt! For Leticha and her mother Mrs Nongayiteni Marinana years of stress and worry have suddenly been lifted from their shoulders. The debts to Foschini and Edcon only totalled R7,189, but to them it seemed like R7 million. “Never, ever, will I buy on credit again,” says Leticha. “I’ve learned my lesson.”

Next: Neighbourhood watch patrollers in Khayelitsha find themselves locked out

Previous: Rubbish piling up in Nelson Mandela Bay

© 2016 GroundUp.

This article is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.

You may republish this article, so long as you credit the authors and GroundUp, and do not change the text. Please include a link back to the original article.